Thursday Thesis #2

APP Earnings, XPER long idea, and my watchlist

Welcome to the 2nd weekly Thursday Thesis! This is not financial advice. Do your own research.

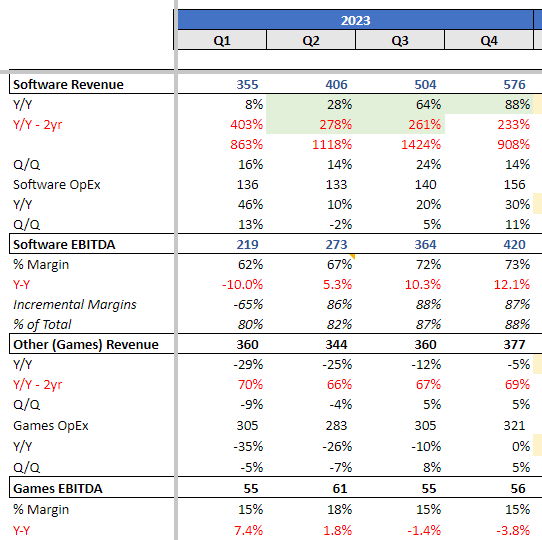

APP | AppLovin 4Q23 EPS

What multiple does the below business deserve in today’s market?

35% Y/Y (and accelerating) revenue growth driven by a transformational AI product.

80%+ incremental EBITDA margins with 70% FCF conversion.

Did I mention AI?

Ignoring the AI part, I’d say 30-40x EBITDA.

It is adtech though, so maybe we should haircut the multiple by 50% to 15-20x EBITDA.

You can buy this business today for just 9x 2024 EBITDA!

End rant…

APP put up a quarter a bit ahead of buyside bogeys and the trend of the past couple of quarters, but as expected continues to climb a wall of worry as investors just hate putting a reasonable multiple on anything adtech.

The Revenue and EBITDA beats were a bit smaller vs. their guidance and Street vs. last quarter as Street continues to bake in more of the upside as APP executes more consistently, but fundamentally everything remains extremely strong.

1Q24 guidance came in nicely above Street which will should take Street 2024/25 numbers a few percent higher, supporting the move after hours.

APP reduced share count by nearly 10% in 2024 and authorized a new $1.25B repurchase plan for another ~7% of shares.

It is worth taking a moment to just acknowledge how insane it is that the Software segment grew 88% with 87% incremental EBITDA margins with a run-rate of $2.3B in annual revenue. APP is growing FCF well over 100% Y/Y and trades at <20x LTM FCF… if this were not branded adtech by investors it would be trading at least at 30-40x EBITDA, and I still believe that is the real upside case here (TTD as the bull case comp who is growing much slower and trading at 4x the multiple).

Rule of 40 could NEVER.

When the intersection of software & adtech works, it works BIG. The question is how long can this combination of insane growth and margins continue and is APP over-earning?

APP’s main business is a bit of a black box B2B product- not something tangible that investors can test out or even that GLG calls can provide a concise explanation of. But the numbers speak for themselves and the return APP provides to their customers has to be dramatically better than Unity and ironSource (U) as they continue to take share despite operating at this insane scale and margin level.

While difficult to diligence, the AXON AI engine just has to be THAT much better. OR is Unity just that bad?

That can all change eventually, and while I am not selling any shares just yet, I am incrementally less excited about the stock over the medium term as I model a bit smaller beats (although still sizable) and as the buyside is increasingly positive (getting crowded, or at least less left-for-dead), as more of my extended buyside network reaches out to talk APP… but I do believe there is a solid chance of the stock really having legs and doubling again from here as it is a dangerous combo of AI, accelerating revenue, and a VERY reasonable multiple.

This key disclosure looked more healthy in Q4- the price x volume breakdown for the Software segment’s growth.

While early 2023 was driven by pricing gains, the business has shifted back into volume growth mode (share gains + market expansion).

My reading of the tea leaves is that this price vs. volume equation tracks to the rollout of AXON 2.0 in early 2023. The release drove a step-function improvement in APP’s targeting capabilities, enabling them to effectively keep more of their partners’ spend on installs while still showing an improving ROI.

As word of this improving ROI spread during 2023 and Unity struggled with their integration of ironSource and developer frustration ramped (distracted competitor), APP began to see accelerating share gains in both new customers and share of budgets.

APP remains my largest position.

Key takeaways from the AppLovin Q4 Earnings call:

When asked about upcoming Google privacy changes - Run a more contextual model than most adtech businesses, so any privacy rule or platform changes may be a relative benefit to APP.

Non-gaming is growing faster than gaming but is smaller.

Starting to see some benefits from non-gaming and CTV, will talk more about it in the coming quarters.

AppLovin’s MAX taps into >1B DAUs, 170M of them in the US. Historically these ad CPMs were extremely low vs. social networks that had sophisticated data and algorithms. With AXON 2.0 APP is getting much more efficient and monetizing these users at a growing level. We are only a couple of quarters into this and it continues to get much better, with a ton of room for growth as the CPMs are starting from a VERY low base.

Compared AXON to ChatGPT getting step-function better with each new model (ie 2.0 → 3.0).

80% incremental EBITDA margins for Software will continue in 2024 (!).

Increased long-term FCF Conversion guidance from 50-60% of EBITDA to 70%.

ROKU + VZIO + XPER | Connected TV Market

I have covered ROKU since its IPO in 2017 when a colleague just about made his career on it.

With rising competition and dramatic valuation discrepancies, I have been meaning to dive into the space and dig into VZIO and XPER.

With WMT’s rumored acquisition of VZIO this week, it looks like I missed that one. However, XPER still looks interesting and the (reported) WMT x VZIO tie-up adds credence to the thesis that competition is likely to dramatically increase over the coming years for incumbent ROKU who has so far just competed with OEM softwares and light competition from Android and Amazon.

VZIO- Walmart controls 37% (!) of US TV sales, and ~70% of VZIO’s sales happen via Walmart with Vizio being the #1 TV brand sold-through there… So the deal makes sense as it helps Walmart tap into that sweet, sweet ad revenue while if VZIO said no, Walmart could destroy their business by cutting their shelf space in half.

While the deal likely leads to VZIO TVs being pushed more in Walmarts (hurting ROKU most directly), it likely also creates more OEM trepidation upon committing to VZIO as an OS partner. That is unless Walmart swings its weight around and forces OEMs to choose the Vizio OS in exchange for better shelf space (I think I recall rumors of WMT using their market power to get Vudu buttons on ROKU remotes years ago).

ROKU- while ROKU continues to command a very strong share of licensed TV OS, competition is on the rise. I have always believed that eventually, ROKU will have to share their advertising economics with their OEM partners, and both VZIO and XPER’s strategies to license their Operating Systems risk pressuring ROKU’s economic model, which has surprisingly shown minimal margins to date.

Both companies seem to have hinted they will be sharing economics with their hardware partners, which I expect to eventually force ROKU to do the same (assuming consumers will not favor competing hardware and choose the TVs with ROKU OS which is a real possibility given their widespread acceptance in the marketplace).

It comes down to whether you think these are differentiated software products that matter to the consumer or are largely commoditized.

I lean towards the latter.

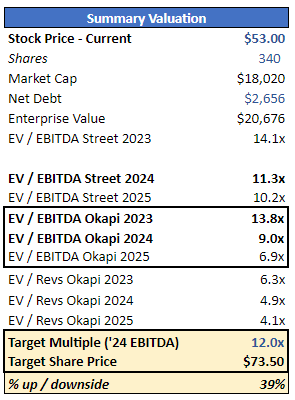

XPER- Enter TiVo (owned by XPER), those good ‘ole & now largely useless set-top-boxes to record your favorite shows. XPER’s business today is largely acting as the OS for cable set-top-boxes, as well as a small hardware business and growing OS businesses for Cars and TVs.

XPER is ahead of VZIO in licensing their OS with TVs with JVC live in the Czech Republic today and multiple OEMs launching in the US in 2024 - early 2025.

XPER expects to have 7M (!) CTV accounts by the end of 2025 based on OEM partners who have already signed up, trades at just 6x Street 2024 EBITDA that should grow dramatically in 2025 if that 7M number is anywhere close to correct and David Rosen of Rubric Capital has recently gone activist on the company (another ex-P72 team, the Cohen Cub mafia is running the CTV OS space).

I’ve begun a starter position in XPER as I dig in further.

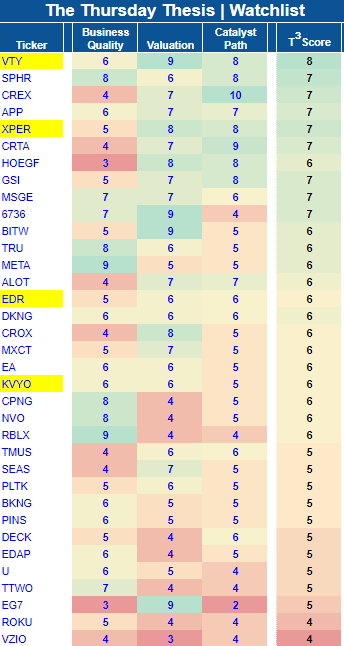

T³ Watchlist

New tickers are highlighted in yellow.

Additions & Changes:

APP- see above. Reduced catalyst path from 9 to 7 after the big earnings beat last night.

XPER- see above.

VZIO- Reduced valuation from 6 to 3 based on WMT deal appreciation. Catalyst path from 6 to 4 as the most meaningful catalyst from here is the deal doesn’t happen and the stock trades towards prior levels.

EDR- Pitch going around for years on Twitter. I have covered EXPE and BKNG for nearly a decade and have always wanted to do a bit of work on EDR. Tim Delaney wrote it up nicely here back in 2021.

EDR is a sub-scale OTA that has pursued a fascinating shift to a subscription model to reduce its reliance on Google leads. The subscription business is growing nicely and management seems able to hit their 2025 targets.

Where this one loses me is the catalyst path and valuation. While the business is certainly becoming higher-quality, management’s target is out there and known. If they hit the 2025 EBITDA target of €180M and the biz is still growing nicely at that point, the stock will work but for this to be a big win you need to bet on relative multiple expansion.

With the stock trading at ~6.5x 2025 EBITDA… unless they blow the target out, this is essentially a bet on multiple expansion. I understand the logic behind subscription being a higher multiple than say EXPE who is overly reliant on Google, but in a relatively sub-scale business like EDR that is a bet I am not willing to make.

VTY- Will discuss more next week… I initiated a large starter position as I dig in. The high-level pitch is almost too good to be true (NVR in the UK with bigger tailwinds & moat), and at a glance, it seems like mostly execution risk.

KVYO- Good write-up from Tech Fund on Twitter. I just can’t get comfortable with the business model. It reminds me of CRTO but rather than being levered to Google/Apple/EU being cool with cookies, they are levered to these companies and regulators being cool with aggressive email marketing practices. Deserves a low multiple in my opinion. Haters will say I just described APP, but they are far more diversified and have even thrived as dramatic privacy changes have rolled out over the past few years.

SPHR- Reduced valuation from a 7 to a 6 as the stock has seen strong follow-through after a solid Q4 report.

HOEGF- Reduced valuation from a 10 to an 8 after strong follow-through post-earnings. A huge catch-up dividend will be paid out in early March (~15% at current levels).

So valuable deep dive. Thank you.

Truly amazing work!